ALSO: Flippers can buy foreclosed homes with FHA loan (up to 4), so it appears residence is not a requirement.

Add up all those numbers and picture is different than you paint (as usual)!!!

I stated the buyers - got an FHA mortgage - made a down payment of just $1,760 - and I wondered if they were going to live there because I assumed (and asked for correction if wrong) that residency was a requirement (re FHA loan)

You replied that they had to pay a higher down payment You replied that foreclosed homes do not require residency

You obviously erred in the amount of down payment they were required to make

I erred in that I thought you were implying this is a foreclosed house when I wondered about residency because the buyers live in NYC but you were merely explaining that foreclosed homes can get FHA loans without residency. So my mistake

But let me ask you, just out of curiousity, is it your understanding that if it's NOT a foreclosure then the FHA would require residency?

In any event, the FHA requires residency for these buyers, but just for a year. Guess that goes against McThief wanting owner occupants as buyers of houses in the city, but I guess he can't necessarily mandate that.

I can't imagine that this house would be a flipper, not selling for $101,000 anyway.

Optimists close their eyes and pretend problems are non existent. Better to have open eyes, see the truths, acknowledge the negatives, and speak up for the people rather than the politicos and their rich cronies.

I stated the buyers - got an FHA mortgage - made a down payment of just $1,760 - and I wondered if they were going to live there because I assumed (and asked for correction if wrong) that residency was a requirement (re FHA loan)

You replied that they had to pay a higher down payment You replied that foreclosed homes do not require residency

You obviously erred in the amount of down payment they were required to make

I erred in that I thought you were implying this is a foreclosed house when I wondered about residency because the buyers live in NYC but you were merely explaining that foreclosed homes can get FHA loans without residency. So my mistake

But let me ask you, just out of curiousity, is it your understanding that if it's NOT a foreclosure then the FHA would require residency?

In any event, the FHA requires residency for these buyers, but just for a year. Guess that goes against McThief wanting owner occupants as buyers of houses in the city, but I guess he can't necessarily mandate that.

I can't imagine that this house would be a flipper, not selling for $101,000 anyway.

I posted the FHA rqmt stating 3.5% down...how would you like further clarification? Here it is again just for you!

Quoted Text

FHA Down Payment Rules One commonly asked FHA loan question involves down payment requirements. Many people want to know what the FHA loan down payment rules are for a particular state or zip code. There's a mistaken impression among some FHA mortgage loan applicants that FHA rules for down payments vary from state to state, but the truth is that FHA loan rules require a minimum down payment of 3.5% for new purchase loans. According to FHA.gov, "Your down payment can be as low as 3.5% of the purchase price, and most of your closing costs and fees can be included in the loan. Available on 1-4 unit properties." One source of the confusion on the down payment issue? Many borrowers find there are additional factors that affect the amount of the down payment. For example, those who do not qualify for the most competitive loan terms may not be able to get the lowest required down payment. Credit issues or other factors may affect the lender's perception of your credit worthiness. That can affect the terms, rates and down payment you're qualified for from that particular lender. Also, participating FHA lenders may also have a higher down payment requirement based on other issues--the FHA minimum isn't a guarantee that you'll be offered that by a particular lender. FHA rules for down payments don't vary from state to state, but the amount of your down payment could vary depending on individual circumstances. Borrowers should not expect to be given the same terms or conditions on an FHA loan as a friend or fellow borrower, and the lender's requirements could vary from loan to loan for a variety of reasons.

ALSO:

Quoted Text

Two mortgage insurance premiums are required on all FHA loans: The upfront premium is 1.75 percent of the loan amount and is paid when the borrower gets the loan but can be financed as part of the loan amount. The second is the annual premium, which varies based on the length of the loan, the amount borrowed and the initial loan-to-value ratio (LTV). The current annual premiums for loans less than $625,500 are: 15-year loan, LTV more than 90 percent: 0.70 percent 15-year loan, LTV 90 percent or less: 0.45 percent 30-year loan, LTV more than 95 percent: 1.35 percent 30-year loan, LTV 95 percent or less: 1.3 percent

Those are the FHA rules, NOT MINE! So don't know how they can do anything different unless there is some additional government subsidy they are using.

Here's the occupancy rqmt:

Quoted Text

FHA Loans and Owner Occupancy There are often questions potential borrowers have regarding FHA loan requirements for occupancy; some borrowers may wish to purchase a home with the idea they will become landlords of that property.

FHA regulations for single-family homes to be purchased with an FHA mortgage have occupancy requirements that prevent this.

FHA loan rules state the borrower applying for a new purchase single family residence must use that residence as the primary occupant or as the "primary residence". But what does the FHA consider a "principal residence" or "primary residence"? Can the FHA approve a second FHA mortgage for those who purchase single-family, owner-occupied property?

The FHA loan rules found in a document known as HUD 4155.1 provide the answer, in the section titled "FHA-Insured Mortgages on Principal Residences and Investment Properties". What follows is the FHA rules for these issues:

"To prevent circumvention of the restrictions on making FHA-insured mortgages to investors, FHA generally will not insure more than one principal residence mortgage for any borrower."

The short answer to these types of FHA loan questions regarding occupancy and renting out the property? If you want to buy a home, the FHA expects you to use it as YOUR home.

Additionally, "FHA will not insure a mortgage if it is determined that the transaction was designed to use FHA mortgage insurance as a vehicle for obtaining investment properties, even if the property to be insured will be the only one owned using FHA mortgage insurance."

To further clarify this issue, FHA loan rules also add, "Any person individually or jointly owning a home covered by an FHA- insured mortgage in which ownership is maintained may not purchase another principal residence with FHA insurance, except in certain situations as described in HUD 4155.1 4.B.2.d." Those types of circumstances should be discussed with an FHA representative and/or your loan officer. Check with FHA if you have circumstances that might be considered eligible for an exception to these FHA loan rules.

It's important to note that borrowers who do not adhere to the FHA occupancy rules could be considered to be acting in "bad faith" on their FHA mortgage loans. Contact your loan officer or the FHA directly to learn what the consequences of acting in bad faith on an FHA loan may be in your state.

JUST BECAUSE SISSY SAYS SO DOESN'T MAKE IT SO...BUT HE THINKS IT DOES!!!!! JUST BECAUSE MC1 SAYS SO DOESN'T MAKE IT SO!!!!!

I posted the FHA rqmt stating 3.5% down...how would you like further clarification? Here it is again just for you!

ALSO:

Those are the FHA rules, NOT MINE! So don't know how they can do anything different unless there is some additional government subsidy they are using.

Here's the occupancy rqmt:

Well, their FHA mortgage DOES require them to occupy the place -- just for one year.

And perhaps you can explain how they made less than the down payment.

Interesting if they had to use additional government TAXPAYER subsidy, just more proof how people do NOT want to buy homes in the city and live in the city -- people need to be bribed to move here Even millionaires won't open up here unless the city hands them millions of taxpayer handouts.

Optimists close their eyes and pretend problems are non existent. Better to have open eyes, see the truths, acknowledge the negatives, and speak up for the people rather than the politicos and their rich cronies.

Well, their FHA mortgage DOES require them to occupy the place -- just for one year.

And perhaps you can explain how they made less than the down payment.

Interesting if they had to use additional government TAXPAYER subsidy, just more proof how people do NOT want to buy homes in the city and live in the city -- people need to be bribed to move here Even millionaires won't open up here unless the city hands them millions of taxpayer handouts.

What part of the post that clearly identifies occupancy requirement did you not understand? Try reading what's been presented before challenging it...if you don't understand the words, then ask the question.....just for you, here's the one sentence that explains it: FHA loan rules state the borrower applying for a new purchase single family residence must use that residence as the primary occupant or as the "primary residence". GOT IT?

As for the down payment, I provided the FHA rules....FHA's, not mine, that state 3.5%....actually it could be even more under certain circumstances. YOU are the one stating they put down less, so why don't you explain how that works, brainiac....you provided the info and I provided the FHA rule. Also, as I stated, there could be other sources and rates could be different. Try reading that info I already posted. So how did they get around the 3.5%, Hero....tell us!

JUST BECAUSE SISSY SAYS SO DOESN'T MAKE IT SO...BUT HE THINKS IT DOES!!!!! JUST BECAUSE MC1 SAYS SO DOESN'T MAKE IT SO!!!!!

News, updates, and explanations to keep you informed.

FHA Loan Down Payment Amounts FHA home loans have plenty of differences from conventional loans, including down payment requirements and the amount of that down payment. When it's time to start planning a budget to cover the costs of an FHA home loan, one of the big questions is "How much down payment should I have saved up?"

These payments depend on percentages. Conventional loan down payment requirements vary from company to company-you may be told by one lender that five percent of the sale price of the home is required, while another may ask for 10%. When it comes to FHA loans, the traditional, bare-minimum down payment amount is 3.5% of the contract sales price of the home. Since FHA down payments are calculated by multiplying the sale price of the home by 3.5%, if you don't know the specific sale price of the home, you won't be able to come up with an exact figure for that down payment.

Figuring out how much to save in the early days of planning requires a bit of simple math--buyers should try to find a price range for homes they want to buy and start saving for the down payment as early as possible, calculating a minimum of 3.5% of the highest figure in that price range just to be safe.

There's no reason why you can't choose a lower amount, but be ready to make up the difference if you find a home you're qualified to buy that has a higher price tag than anticipated. The reverse is also true--FHA mortgage loan applicants can put more money on their down payment in order to lower monthly mortgage bills-there is no requirement that the borrower must only pay the 3.5% minimum. One important detail to be aware of--the FHA requires down payments be made by the buyer. The seller is allowed to offer concessions such as paying closing costs or other expenses related to selling the home, but the seller is prohibited from contributing a down payment.

The buyer must provide the funds for the down payment and other up-front costs do not count towards the down payment amount. That's one reason why a long period of planning and saving is recommended for those who want an FHA mortgage or a conventional home loan.

JUST BECAUSE SISSY SAYS SO DOESN'T MAKE IT SO...BUT HE THINKS IT DOES!!!!! JUST BECAUSE MC1 SAYS SO DOESN'T MAKE IT SO!!!!!

FHA Loan Requirements •Must have a steady employment history or worked for the same employer for the past two years •Must have a valid Social Security number, lawful residency in the U.S. and be of legal age to sign a mortgage in your state •Must make a minimum down payment of 3.5 percent. The money can be gifted by a family member. •New FHA loans are only available for primary residence occupancy •Must have a property appraisal from a FHA-approved appraiser •Your front-end ratio (mortgage payment plus HOA fees, property taxes, mortgage insurance, home insurance) needs to be less than 31 percent of your gross income, typically. You may be able to get approved with as high a percentage as 46.99 percent. Your lender will be required to provide justification as to why they believe the mortgage presents an acceptable risk. The lender must include any compensating factors used for loan approval. •Your back-end ratio (mortgage plus all your monthly debt, i.e., credit card payment, car payment, student loans, etc.) needs to be less than 43 percent of your gross income, typically. You may be able to get approved with as high a percentage as 56.99 percent. Your lender will be required to provide justification as to why they believe the mortgage presents an acceptable risk. The lender must include any compensating factors used for loan approval. •Minimum credit score of 580 for maximum financing with a minimum down payment of 3.5 percent. •Minimum credit score of 500-579 for maximum LTV of 90 percent with a minimum down payment of 10 percent. FHA-qualified lenders will use a case-by-case basis to determine an applicants' credit worthiness. •Typically you must be two years out of bankruptcy and have re-established good credit. Exceptions can be made if you are out of bankruptcy for more than one year if there were extenuating circumstances beyond your control that caused the bankruptcy and you've managed your money in a responsible manner. See this page for more details. •Typically you must be three year out of foreclosure and have re-established good credit. Exceptions can be made if there were extenuating circumstances and you've improved your credit. If you were unable to sell your home because you had to move to a new area, this does not qualify as an exception to the three-year foreclosure guideline.

JUST BECAUSE SISSY SAYS SO DOESN'T MAKE IT SO...BUT HE THINKS IT DOES!!!!! JUST BECAUSE MC1 SAYS SO DOESN'T MAKE IT SO!!!!!

What part of the post that clearly identifies occupancy requirement did you not understand? Try reading what's been presented before challenging it...if you don't understand the words, then ask the question.....just for you, here's the one sentence that explains it: FHA loan rules state the borrower applying for a new purchase single family residence must use that residence as the primary occupant or as the "primary residence". GOT IT?

As for the down payment, I provided the FHA rules....FHA's, not mine, that state 3.5%....actually it could be even more under certain circumstances. YOU are the one stating they put down less, so why don't you explain how that works, brainiac....you provided the info and I provided the FHA rule. Also, as I stated, there could be other sources and rates could be different. Try reading that info I already posted. So how did they get around the 3.5%, Hero....tell us!

I initially commented that I wondered if they would live in it since it was not anyone local, curious whether people could buy a house with an FHA loan and not live in it.

You answered that about the FHA allows flippers to buy up to four with an FHA loan, so you answered that, I and thus I fully comprehend and understand that (though I can't imagine most taxpayers would agree with the government allowing that but we won't get into that).

But discussion/understanding of occupancy in this case is a moot issue somewhat because their FHA mortgage mandates occupancy/primary residency in this case, though only for one year (which kind of surprises me).

I'm not saying I don't believe you about the 3.5% down, I know they are not your rules, I'm just stating the fact right from the mortgage document itself. Your reference to possibly some other provision, do you happen to know if they could have paid, perhaps 5% down (roughly $5,000) and then maybe the closing costs were $5,000 so they included the closing costs in the mortgage? We've never had experience with dealing with the FHA or any of those government mortgages.

But the bigger issue is a huge house, very nice (for those who like that style), takes two years to sell, selling for just about 50% less than the city claims it would sell for, with a taxes calculated at a value that is 80% higher than the house is worth; actually they will pay almost twice the taxes that they should pay.

Optimists close their eyes and pretend problems are non existent. Better to have open eyes, see the truths, acknowledge the negatives, and speak up for the people rather than the politicos and their rich cronies.

Your down payment can be as low as 3.5% of the purchase price, and most of your closing costs and fees can be included in the loan.

Quoted Text

Two mortgage insurance premiums are required on all FHA loans: The upfront premium is 1.75 percent of the loan amount and is paid when the borrower gets the loan but can be financed as part of the loan amount. The second is the annual premium, which varies based on the length of the loan, the amount borrowed and the initial loan-to-value ratio (LTV). The current annual premiums for loans less than $625,500 are: 15-year loan, LTV more than 90 percent: 0.70 percent 15-year loan, LTV 90 percent or less: 0.45 percent 30-year loan, LTV more than 95 percent: 1.35 percent 30-year loan, LTV 95 percent or less: 1.3 percent

I still want to see that they put down less than the required amount!

JUST BECAUSE SISSY SAYS SO DOESN'T MAKE IT SO...BUT HE THINKS IT DOES!!!!! JUST BECAUSE MC1 SAYS SO DOESN'T MAKE IT SO!!!!!

Good one...I'll remember this....MC1 the PUBLIC SERVANTS, Robin Hoods of Schdy!!!!!

And real estate agents!

We are advised NOT to judge ALL Muslims by the actions of a few lunatics, but we are encouraged to judge ALL gun owners by the actions of a few lunatics. Funny how that works.

I still want to see that they put down less than the required amount!

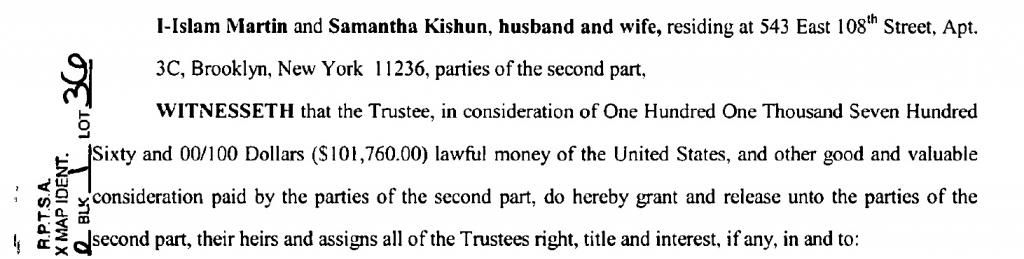

First image is from the deed, you can CLEARLY see the price paid which agrees with the deed stamps of 408.

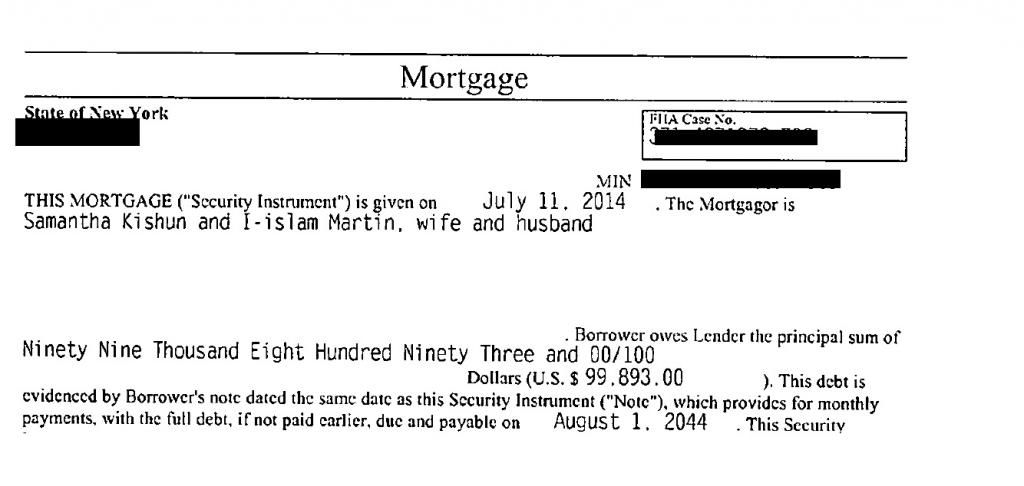

Here is from the FHA mortgage, showing the amount of the mortgage

So based on the purchase price from official government documents (NOT a tabloid website) and the amount of the FHA mortgage document itself, the math is

But yes, like you posted something, people can mortgage their closing costs. Like I said, I'm not thoroughly familiar with FHA mortgages other than it's government (taxpayer). But can people getting these mortgages have money in their hands for closing costs but instead use that money to define it as a down payment just to qualify for an FHA mortgage (when they get turned down for a normal mortgage) and then just mortgage their closing costs?

Optimists close their eyes and pretend problems are non existent. Better to have open eyes, see the truths, acknowledge the negatives, and speak up for the people rather than the politicos and their rich cronies.

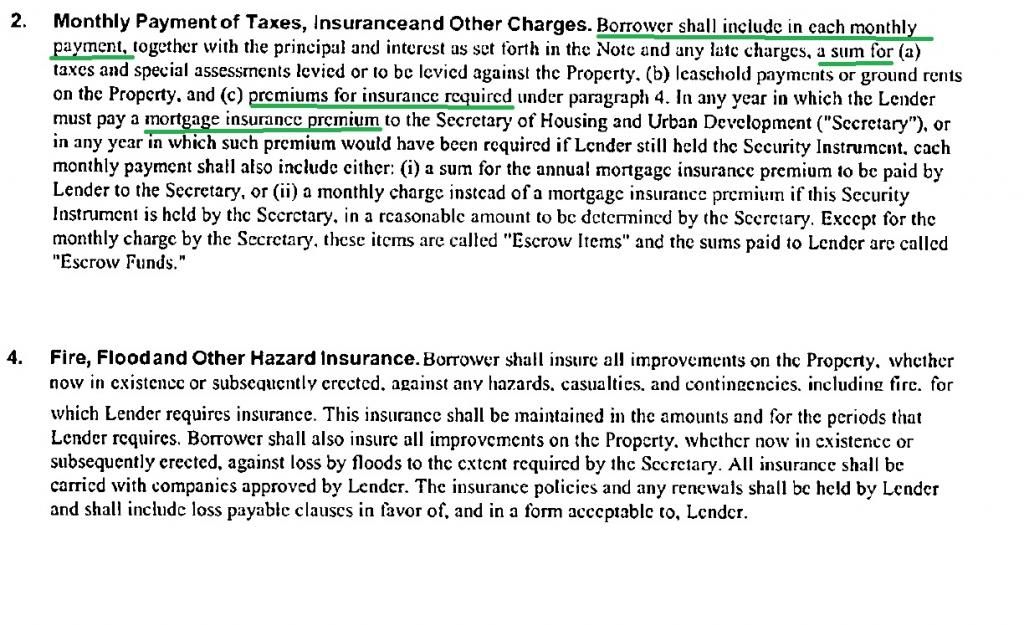

something is missing because it doesn't show insurance either. They could have paid for both insurance closing costs out of pocket but that wouldn't lower the req'd down payment. Data has to be missing.

JUST BECAUSE SISSY SAYS SO DOESN'T MAKE IT SO...BUT HE THINKS IT DOES!!!!! JUST BECAUSE MC1 SAYS SO DOESN'T MAKE IT SO!!!!!

I don't see anything wrong with being concerned about this issue. If more people had been concerned sooner, we wouldn't have had the 2008 financial collapse, which we all paid for, some of us more than others. If the family in my neighborhood who already has a house up for sale they just bought a couple years ago had gotten better information, maybe they wouldn't have purchased a home they could not really afford. If more people had woken up to the tax situation in Schenectady, things might have been rectified before some of these people lost their houses. The situation with this house that was finally sold, on our dime? I don't see anything wrong with someone who has a stake in the city, being concerned as to just what sort of deal transpired. The rest of you, apparently in favor of ignorance, look away.

something is missing because it doesn't show insurance either. They could have paid for both insurance closing costs out of pocket but that wouldn't lower the req'd down payment. Data has to be missing.

Insurance is escrowed. Required to have both mortgage insurance and homeowners insurance.

Optimists close their eyes and pretend problems are non existent. Better to have open eyes, see the truths, acknowledge the negatives, and speak up for the people rather than the politicos and their rich cronies.

Insurance is escrowed. Required to have both mortgage insurance and homeowners insurance.

Primary insurance is upfront cost that has to be either paid at closing or included in mortgage, not escrow! I posted before:

Quoted Text

Two mortgage insurance premiums are required on all FHA loans: The upfront premium is 1.75 percent of the loan amount and is paid when the borrower gets the loan but can be financed as part of the loan amount.

JUST BECAUSE SISSY SAYS SO DOESN'T MAKE IT SO...BUT HE THINKS IT DOES!!!!! JUST BECAUSE MC1 SAYS SO DOESN'T MAKE IT SO!!!!!

Primary insurance is upfront cost that has to be either paid at closing or included in mortgage, not escrow! I posted before:

OK, yes, I agree, but afterwards insurance IS escrowed

At closing you pay the full year's premium of homeowners' insurance. And maybe the PMI as well. Then from that point on, every month part of your monthly payment goes into escrow earmarked for insurance.

And the mortgage insurance is paid every month by the bank to the company with the mortgage insurance.

Optimists close their eyes and pretend problems are non existent. Better to have open eyes, see the truths, acknowledge the negatives, and speak up for the people rather than the politicos and their rich cronies.

Logged

Logged